From its real name "The Descartes Systems Group", the company was born some forty years ago near Toronto. It is a specialist in supply chain software. Its ecosystem includes solutions for route and transport planning, inventory and warehouse management, business-to-business dialogue and sales data optimization. These tools are designed to facilitate both long-distance cross-border trade and the complex issue of the last mile. Users of the Group's solutions fall into two main groups. On the one hand, logistics service providers such as airlines, railways, road haulage companies and forwarding agents. On the other, their customers - producers, wholesalers, retailers and Internet retailers. It goes without saying that the need for logistics optimization has exploded in recent years, with the growth of online business. The best e-commerce sites are those that are able to respond most rapidly to the demands of consumers now accustomed to having their desires fulfilled in record time.

The last shall be first

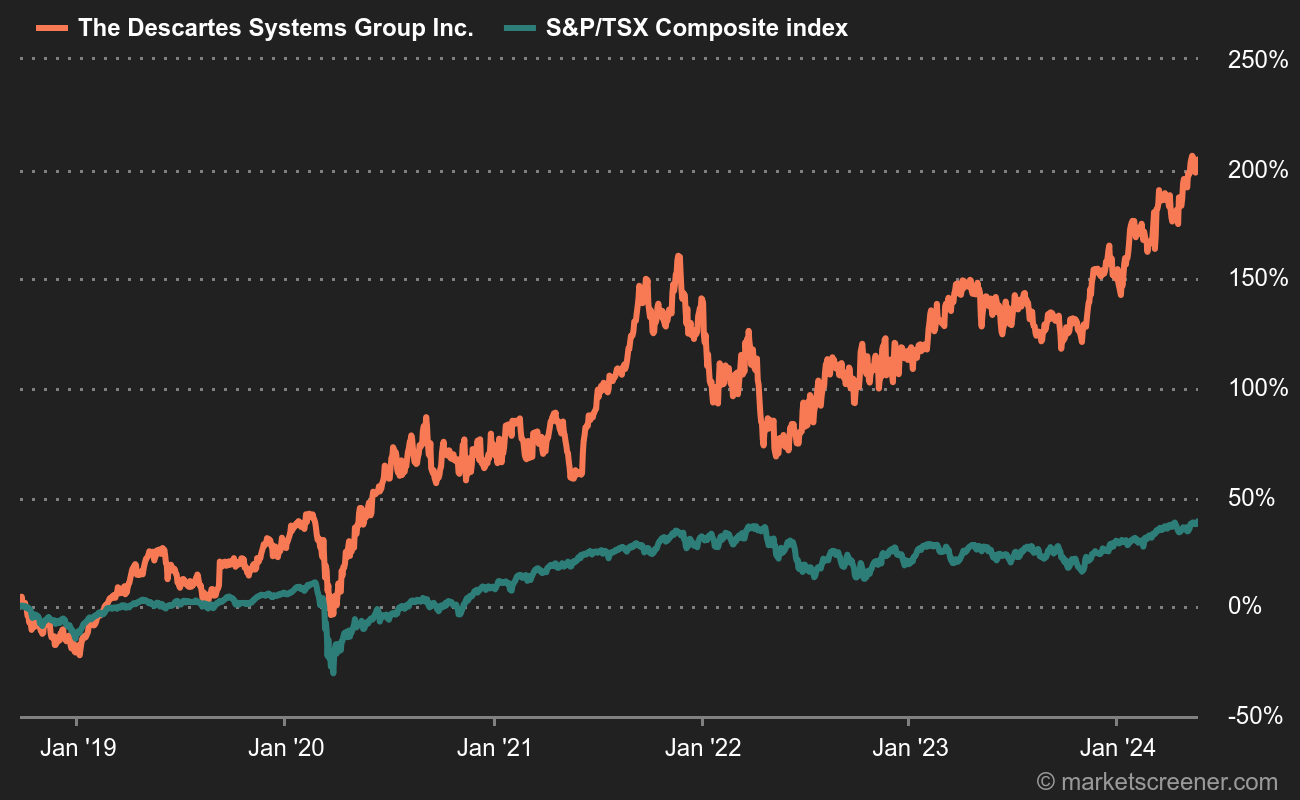

Before becoming a "logical and rational" machine, Descartes almost went bankrupt in the early 2000s. Twenty years later, the Canadian group has become a model of fastidious management, having pioneered the use of software on demand, or SaaS, to enhance its offering. Like many companies in the technology sector, the group has deployed an aggressive acquisition policy known as roll-up. This involves agglomerating small companies operating in identical, related or geographically complementary sectors, in order to grow and offer a broader range of products and services. This strategy has been crowned with success, as it has enabled Descartes to become one of the world's leading players in its field. It should be stressed that shareholders have not been excessively solicited over the last ten years to build this edifice, despite two fund-raising operations. Moreover, they have no reason to complain about the company's external growth policy, since the return on invested capital is quite satisfactory by financial standards.

Cash machine

The business model, based on cloud computing, is now well established. With the exception of a slight contraction in 2018, free cash flow has grown steadily over the past ten years.

| Fiscal Period: January | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 |

|---|---|---|---|---|---|---|---|---|

| Net sales 1 | 325.8 | 348.7 | 424.7 | 486 | 572.9 | 633 | 699.2 | 767.7 |

| EBITDA 1 | 122.6 | 142 | 185.7 | 215.2 | 247.5 | 280.2 | 314.1 | 348.8 |

| EBIT 1 | 52.26 | 71.4 | 103.4 | 130.4 | 142.8 | 192.5 | 224.2 | 267.7 |

| Operating Margin | 16.04% | 20.48% | 24.36% | 26.84% | 24.93% | 30.42% | 32.07% | 34.87% |

| Earnings before Tax (EBT) 1 | 48.04 | 70.37 | 102.6 | 133.7 | 151.2 | 202 | 237.1 | 271.7 |

| Net income 1 | 37 | 52.1 | 86.28 | 102.2 | 115.9 | 148.2 | 171.6 | 198.9 |

| Net margin | 11.36% | 14.94% | 20.32% | 21.04% | 20.23% | 23.41% | 24.54% | 25.91% |

| EPS 2 | 0.4500 | 0.6100 | 1.000 | 1.180 | 1.340 | 1.709 | 1.961 | 2.307 |

| Free Cash Flow 1 | 99.35 | 127.5 | 171.3 | 186.3 | - | 222.3 | 265.1 | 306 |

| FCF margin | 30.5% | 36.56% | 40.34% | 38.34% | - | 35.13% | 37.91% | 39.86% |

| FCF Conversion (EBITDA) | 81.04% | 89.77% | 92.25% | 86.58% | - | 79.35% | 84.38% | 87.74% |

| FCF Conversion (Net income) | 268.54% | 244.67% | 198.55% | 182.25% | - | 150.06% | 154.45% | 153.82% |

| Dividend per Share | - | - | - | - | - | - | - | - |

| Announcement Date | 3/4/20 | 3/3/21 | 3/2/22 | 3/1/23 | 3/6/24 | - | - | - |

In the last financial year, which ended on March 31, Descartes generated sales of US$486 million, net income of $102 million and free cash flow of $186 million. Descartes' status as a high-margin, recurring software publisher translates into generous valuation multiples based on net income, but more affordable based on free cash flow, which is an excellent indicator of the company's true cash-generating capacity. At the same time, the balance sheet is extremely solid, with a positive net cash position that has persisted for years, meaning that cash on hand exceeds (by a wide margin, in this case) debts.

If the earnings trajectory anticipated by analysts is confirmed, and Descartes continues to stick to its business plan, investors will find this an interesting technology story, proving that the USA does not have a monopoly on software success stories.