Cavco is one of those companies that recorded an exceptional stock market performance over a period of about 20 years. Recognition of quality over such a long period of time cannot be due to chance, and we will try to understand the reasons for this success.

Source: MarketScreener - Chart

Cavco has been benefiting from rising real estate prices for over 10 years in the United States. Today, it is one of the largest US HUD builders with 31 production lines. First, a growing population and a generally stable economy have led to a steady rise in housing demand. In addition, there aren't enough houses for sale because housing supply hasn't kept up with demand. Due to greater buyer rivalry, prices have risen as a result. Low interest rates and liberal lending requirements have also made it simpler for people to get mortgages and buy homes, which has increased demand. Finally, the tendency of individuals relocating from urban regions to suburban and rural areas has been increased by the COVID-19 epidemic, which has raised the price of properties outside of large cities and increased demand for those types of residences.

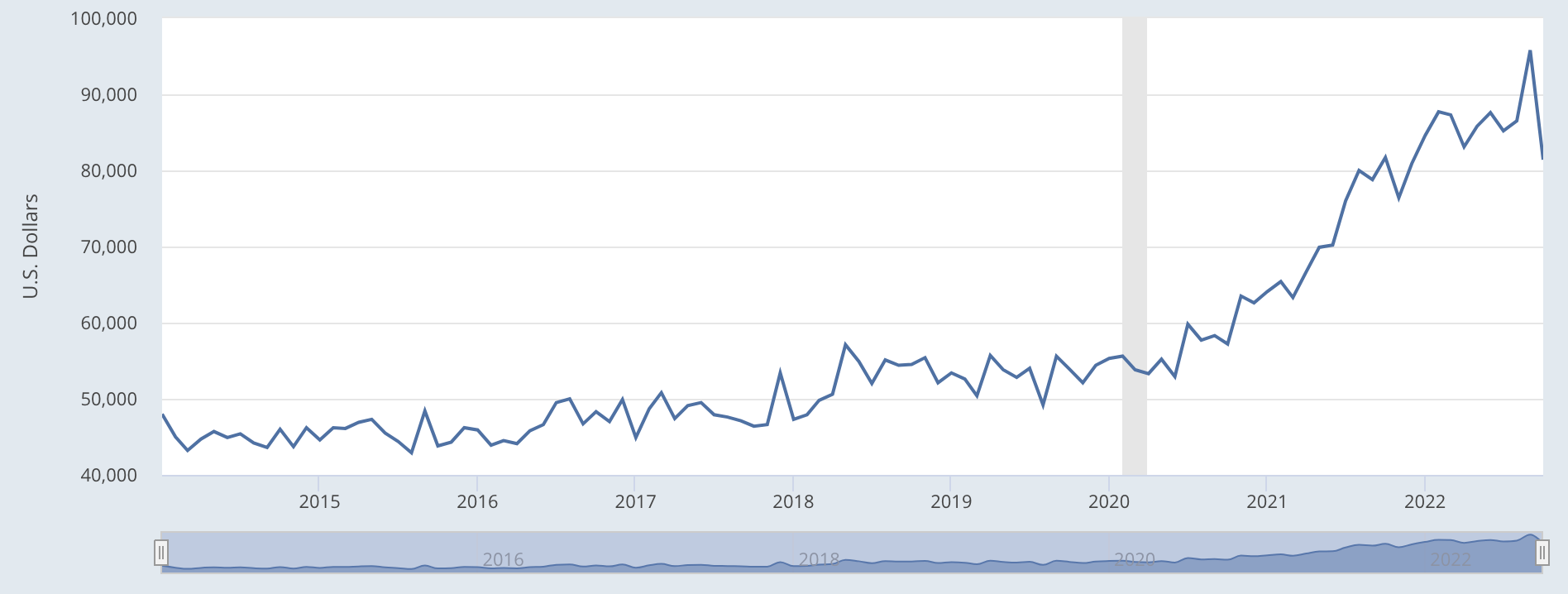

Source: US Census Bureau; Federal Reserve Bank of St. Louis - Average Sales Price of New Manufactured Homes: Single Homes in the United States

Cavco has two distinct businesses. On the one hand, the manufactured housing sector (wholesale and retail sales) accounts for 95.6% of sales and is up 49.95% between 2021 and 2022, while the financial services sector (consumer financing and insurance for manufactured housing) accounts for 4.4% of sales over the same year and has only grown by 1.02% over the same period. The company primarily distributes its manufactured homes through independent and company-owned retailers, planned community operators and residential developers, which account for the majority of the group's revenues.

In recent years, there has been a marked increase in costs, such as wood, metals and labor. Manufactured housing producers like Cavco passed these costs on to buyers, significantly increasing their margins and profits. While the manufactured housing industry has historically been cyclical, there is a strong offer for affordable housing since job growth allowed more buyers to buy premium houses. And, despite these economic cycles Cavco should thrive because of its low prices, variable cost structure, controlled manufacturing environment and the fact that there is no land risk. Cavco focuses on producing 4 different types of Superior Homes such as the HUD-Code Home; Modular Home; Park Model; Multi-family/Commercial while distributing these properties through 3 distribution channels: Retail; Builder/Developer and Communities.

Source: Cavco - Products

Quality acquisitions:

Cavco Homes' M&A activities have had a positive impact on the business, particularly in terms of expanding its geographic reach and product offerings. The acquisition of Nationwide Homes in 2016 granted Cavco Homes entry to the previously untapped East Coast market, while the acquisition of Chariot Eagle in 2019 expanded the company's product range to include luxury park model RVs, catering to a wider customer base. The company purchased Commodore in 2021 (which added six new manufacturing facilities), which is the largest independent producer of manufactured housing in the US, allowing Cavco to expand in the Northeast while strengthening its position in the Midwest and Mid-Atlantic markets. And, more recently in January 2023, Cavco acquired Solitaire Homes to strengthen position in the Southwest as well as it commenced operations at new park model manufacturing facility

Those acquisitions helped Cavco Homes to achieve operational efficiencies and cost savings through economies of scale. By acquiring companies with established manufacturing facilities and distribution channels, Cavco Homes has been able to leverage its resources more effectively, leading to improved margins and profitability.

This financial strategy has ensured organic growth, capacity expansion and shareholder value over the past 12 years, resulting in continued revenue and profit growth. In 2022, the company has committed $244 million for strategic acquisitions and $52 million for internal projects.

Source: Cavco - Brand Portfolio

Valuation:

Over the last decade (2013-2023) we see the company paying itself less and less "expensive" to find some equilibrium around 11-12x. At the same time, with a valuation of more than 65x its earnings in 2013, Cavco was very (if not too) expensive compared to its competitors and the market. The ROA (Return on Asset) has doubled between 2019 and 2022 from 10% to 20% and the ROE (Return on Equity) has also doubled over the same period, from 13.9% to 28.3%.

The stock is attractive, as evidenced by its steadily increasing revenues. Analysts are forecasting $2.1 billion in revenues for 2023, an increase of 382% since 2013 (CAGR of 11.39%). At the same time, the operating margin has risen above 10% (12.4% in 2022), the first time this has happened in 10 years, which shows the group's very good management. Cavco also benefits from one of the highest gross margins in the sector, at 26%. Above all, Cavco has seen its net income soar by almost 3900% since 2013. The company can also take advantage of its earnings per share (EPS), which have increased by 187% over the last three years.

The earnings release for the second quarter of 2023 was quite good with a rise in gross profit to 27.3% as well as an increase in earnings per diluted share to $8.25 and a net income of $577 million. However, one must be careful with earnings per share (EPS) which, according to various analysts, are expected to decline over the next three years. After having risen steadily to reach $21.3 in 2022, forecasts announce an EPS of $23 for 2024 and 2025. This decline can be explained by a decrease in future revenues or an increase in the price of basic materials that the company is unable to translate into sales prices. At the same time, the macro-microeconomic situation (inflation) and current monetary policy is complicated with key interest rates that continue to rise. This situation will undoubtedly be complicated for Cavco, where customers will not necessarily be able to afford to buy prefabricated house at a price they "consider" too expensive.

Conclusion:

Cavco is positioned in a sustainable and growing market. The average price of real estate in the United States has more than doubled since the subprime crisis, demonstrating the attractiveness of the United States to institutions and individuals. Several studies estimate an increase of 3-5% per year until 2030. Cavco has a solid track record and its earnings reports, although sometimes irregular, are well received by investors. It will be important to monitor the company's ability to continue its growth, such as attacking the international market (which has not yet been done), but which is undoubtedly the future growth driver, as well as continuing to offer attractive prices. However, be careful not to look only at past performance because it does not guarantee future performance. The real estate market is currently in a delicate situation (somewhat similar to 2008)