|

Friday July 24 | Weekly market update |

|

Financial markets just had a turbulent week and are on the way to finishing close to their weekly lows, caught up by the renewed tensions between China and the United States and the results of US technology stocks. Operators opted for clear profit-taking, amid the ongoing Covid-19 outbreak, as companies unveil cautious outlooks. |

| Indexes Over the past week, the Nikkei gained 0.2%, as the Japanese stock market remained closed on Thursday and Friday. The Hang Seng lost 1.6% while Shanghai Composite gained 2.3%, despite the reciprocal closure of a Chinese and then an American consulate, intensifying tensions between the two countries. In Europe, contrary to the previous week, all indices lost ground. The CAC40 fell by 2.6%, the Dax by 0.5% and the Footsie by 2.3%. Spain lost 2.3%, Portugal 0.1% and Italy 1.8%. In the United States, at the time of writing, the Nasdaq100 was down 1.5%, the Dow Jones 1.2% and the S&P500 0.3%. Nasdaq100  The index is testing its bullish streak that began in mid-March. |

| Commodities Oil prices flattened over the past few days. This astonishing stability is the consequence of a lack of visibility on the behavior of demand in the coming months due to the spread of the virus around the world. The slow recovery of OPEC+ supply is also weighing on buying initiatives. As a result, the market has found a balance in these price zones (USD 43 for Brent and USD 41 for WTI) and is not moving away from them while waiting for new catalysts. Precious metals, on the other hand, are gaining momentum. Gold is attracted by its historical record above USD 1900, while silver has set a new record at 21%. The grey metal has actually gained 17% over the last five days. Industrial metal prices are on the rise again, supported by the weakness of the greenback and the absence of bad news on the Chinese economic statistics front. Copper returns above USD 6500 while tin accelerates to USD 17760. |

| Equities markets NEL Founded in 1927, NEL is a Norwegian company specialising in hydrogen, including the manufacture of electrolysers and hydrogen filling stations. In the current context of energy transition, the Oslo-based company may well benefit from the hydrogen trend, which is still not very democratic. The multiple recovery plans of the world economies, following the health crisis, promote sustainable development. With an investment rate of over 20% of turnover (€53.8 million) in 2019, Nel intends to position itself for growth. The company has seen its turnover almost double between 2017 and 2019, it could reach €67 million in 2020. Profitability is improving even if net income is expected to remain in the red (-14 million euros), which gives the share few assets in terms of valuation. Traded on the Oslo Stock Exchange for 15 years, the share has risen by more than 145% since the beginning of the year, bringing the company's market capitalisation to €2.8 billion. Admittedly, the share price is still a long way from its historical highs (NOK 230 as opposed to NOK 18 today). Investors have returned massively to the Nel share over the last few years.  |

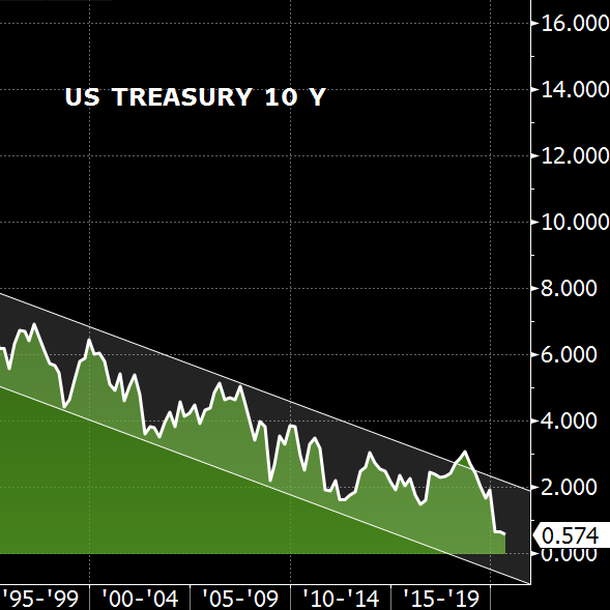

| Bond market Government bond spreads have narrowed across broad segments of the curve. The factor behind this development continues to be the agreement reached by the European Council on the EUR 750 billion EU Reconstruction Fund. This financial firepower has therefore eased overall yields. The Bund saw its rate fall to -0.48% and the OAT to -0.18%. The reduction in spreads has benefited the southern countries, such as Italy, which can now borrow at ten years, below 1%, and Spain at 0.32%. The Italian government will soon benefit from this as it plans to borrow up to EUR 25 billion to finance the repercussions of the pandemic in 2020. Still in Europe, there has been little change in the Swiss 10-year loan, which provides a largely negative return of -0.55%. In the United States, investors are taking some profits on equities and are moving towards the bond market since the yield on the Tbond has fallen to an all-time low of 0.55%. U.S. 10-year at an all-time low  |

| Forex market The Franco-German collective loan project was finally adopted by the European Union. This 750 billion euro recovery plan will be financed for the first time by a joint debt. It includes €390 billion in non-repayable grants and €360 billion in loans. This agreement has had the effect of reducing interest rate spreads in the euro zone and of subsidising the single currency up to USD 1.16. The graph shows an acceleration of the EUR/USD exchange rate, which has returned to more treated levels since October 2018. The current trend could take the single currency to the 1.18 USD zone. In Australia, retail sales posted a 2.4% increase in June, after jumping 16.9% in May. This good figure is explained by the lifting of lockdown and the reopening of shops. The AUD, a currency that often measures the market's appetite for risk, rose against its main counterparts and is trading at 0.71 against the greenback. The yen lost ground in this less stressed environment, particularly against the euro (JPY 124), an increase of 250 basis points. However, if the deterioration in China-U.S. relations continues, safe haven currencies such as the Japanese currency and the Swiss franc should be favored by Forex traders. Strong rise of the single currency against the dollar  |

| Economic data In Europe, macroeconomic data has been reassuring, especially with the agreement on the European Recovery Fund. The Flash PMI manufacturing and services indices exceeded expectations, at 51.1 and 55.1 respectively (consensus 50 and 51), reflecting an expansion of economic activity. Next week will be denser, with Germany's IFO, import and consumer prices, GDP and retail sales. For the Euro-Zone, traders will take note of the Unemployment Rate, CPI and GDP next Friday. Across the Atlantic, all figures missed the consensus. Existing Home Sales came out at 4.72M vs. 4.77M expected and New Home Sales at K. Oil inventories rose to 4.9M and weekly listings rose for the first time since the deconfinement (1416K vs. 1300K expected and 1307K last week). For the Flash PMI manufacturing and services indexes, they come out at 51.3 and 49.3 (against 52 and 51 expected). Starting Monday, the following will be released: durable goods orders, the Conference Board index, GDP, unemployment registrations, household spending and income, and the Michigan confidence index. The Fed will also deliver its monetary policy verdict on Wednesday. |

| The equation gets complicated The dichotomy between the economy and equity markets persists, despite the return of strong geopolitical tensions between China and the United States. Since the health crisis, investors have favoured more tactical allocations that reflect discriminatory behaviour within the indices. The winning sectors maintain their hegemony over the sector sub-funds that were more affected by the health crisis, even though the latter are experiencing a revival during certain stock market episodes. The world is changing and the future remains a mystery, with marked earnings revisions over 2020, which implies a strict stock-picking mode on the part of investors. The looming US elections should not favor a Sino-American lull. This new unknown could further complicate the current equation. |