|

Monday May 3 | Weekly market update |

| Good corporate results and the Federal Reserve's continued ultra-accommodating monetary policy have kept the buying current going last week, allowing many indices to set new annual or even historic records. However, some profit-taking occurred on Friday, as interest rates have risen again, with inflation rising in the United States and Germany. |

| Indexes Over the past week, Asia has lagged, with the Nikkei losing 0.7%, the Shanghai Composite 0.8% and the Hang Seng down 1.2%. In the euro zone, the CAC40 recorded a weekly performance of 0.45%. The Dax is down 0.6% while the Footsie is up 0.6%. In the peripheral countries, Italy is down 0.9%, while Portugal and Spain are the two best performers, with +1.45 and 2.7%. In the United States, the Dow Jones is down 0.5% over the last five days, the S&P500 is down 0.2% and the Nasdaq100 is stable. |

| Commodities Oil prices signed a beautiful week of progression, supported by a fall of American stocks. The status quo of OPEC+, which unsurprisingly maintained its strategy. The gradual increase in supply from the enlarged cartel did not destabilize operators. As a result, Brent crude oil rose to 68.4 USD per barrel, while WTI was close to 65 USD on Friday. Precious metals fell sharply after Jerome Powell's speech, which anchored market expectations of a no-deal inflationary scenario. Gold lost ground to USD 1760, as did silver to USD 27.7. It was the event of the week, the ton of copper reached USD 10,000 on the LME, a level not seen since 2011. The red metal, considered a barometer of the global economy, is a victim of a very high demand. Most of it is coming from China, and supply is not keeping pace. Copper accelerates  |

| Equities markets A Swedish company specialized in the virtualization of casino gaming rooms, Evolution Gaming Group started in 2006 to provide table monetization services for its clients: 888 Casino plus other well-known brands such as Betfair, Betsson, Draftkings, Unibet. EGG operates as a subcontractor that develops, produces and licenses technology for the reproduction of virtual gaming rooms. The company has benefited greatly from the closure of casinos during the pandemic. The presentation of the Q1 2021 results has been welcomed by investors: +18% in the last five days. The short-term (+101% since January 1), medium-term (+537% since the March 2020 low) and long-term (+2,866% over five rolling years) variations are impressive, as shown in its chart below. Evolution Gaming Group stock surges  |

| Bond market Pointing to a marked improvement since the pandemic took hold more than a year ago, the Fed said that "risks to the economic outlook remain," softening previous language that referred to the virus posing "considerable risks." Following this intervention, yields on US 10-year Treasuries returned to the upside, at 1.63%. In Europe, bond benchmarks are offering more attractive returns. While the German Bund remained in negative territory (-0.22%), other major bonds on the continent posted positive rates, such as the French OAT at 0.12%. Italy (0.88%), Spain (0.44%) and Greece (0.94%) are also seeing their main debt offer higher yields. The upward trend in yields on sovereign securities is also duplicated for the Swiss 10-year bond, which is back near zero at -0.25%. |

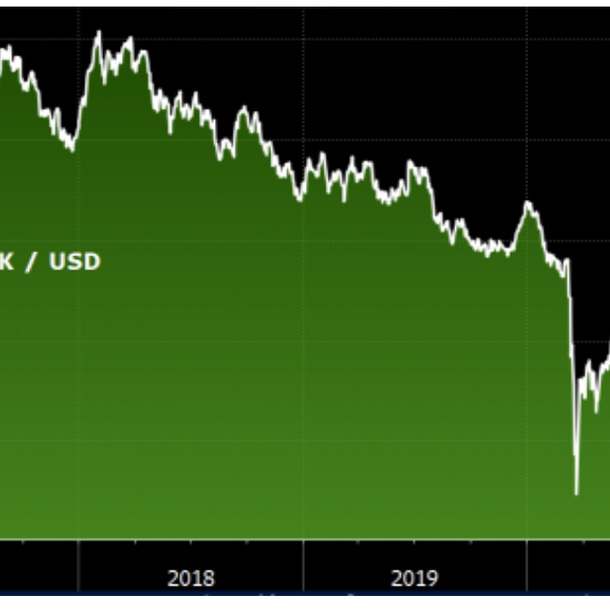

| Forex market In the U.S., the White House's announcement of a potential tax increase, including a tax on gains from financial transactions, has pushed the greenback onto the defensive. Investors turned away from the dollar to buy the single currency. In the U.K, the Purchasing Managers' Index reflected the fastest growth in the UK private sector since late 2013. The pound took advantage of this publication to gain a few basis points against the dollar to 1.40 USD. Propelled by the current tensions on commodity prices, the Canadian dollar posted a 4-year high against the dollar at USD 0.813. In Europe, the Norwegian krone continued its winning streak. The Nordic currency has jumped 7% against the euro in the last 4 months. Forex traders remain "long" on the NOK and anticipate, at the dawn of the end of the global crisis, an upcoming rate hike by the Norge Bank. For their part, the Swiss franc and the yen, traditional targets of safe-haven flows, are in retreat in a market where investors have put the "risk" cursor at the maximum gauge. Norwegian krone rises against the greenback  |

| Economic data In China, few data were on the agenda. The manufacturing and services PMI indices came out at 51.1 and 54.9 respectively (compared to 55.9 and 51.8). For once, growth in manufacturing activity is slowing down while that of services is accelerating. For Germany, the IFO fell to 96.8 (versus 97.8 expected) and GDP declined by 1.7% (consensus -1.5%). On the other hand, import prices rose by 1.8% and the German CPI index came in at 0.7%. In the euro zone, most figures exceeded expectations. The unemployment rate fell to 8.1%, GDP declined by only 0.8% and the consumer price index was within consensus at +1.6%. In the U.S, the data mostly disappointed. While the Conference Board index peaked at 121.7 and household spending jumped by 21.1%, spending only climbed by 4.2%. GDP was slightly below expectations (6.4% vs. 6.8% expected) and weekly jobless claims were worse than expected at 553K. Trade Balance, Pending Home Sales and Wholesale Trade Inventories also disappointed. |

| Hope keeps indexes in orbit It's a strange atmosphere around indexes, which are not necessarily showing any technical acceleration, but are not giving up any ground. This situation of slow ascent, recording day after day historical records, is done with a collapse of the volatility which touches lows since the period before the health crisis. The first quarter was exceptional in terms of earnings reports. The vigorous recovery should continue over the next few quarters, especially if consumption regains a dynamic position alongside investment, the pillars of solid growth. The major question now lies in the economy's ability to withstand this demand shock and therefore overheating (like the tensions on commodity prices), without generating a lasting increase in prices beyond a temporary phenomenon. |