S&P 500

S&P 500

The Bottom Line:

- Shifts to consumer discretionary and technology stocks after the purge.

- Growth is making a comeback, but value is not abdicating.

- Industrial metals lag energy.

- The euro is waking up.

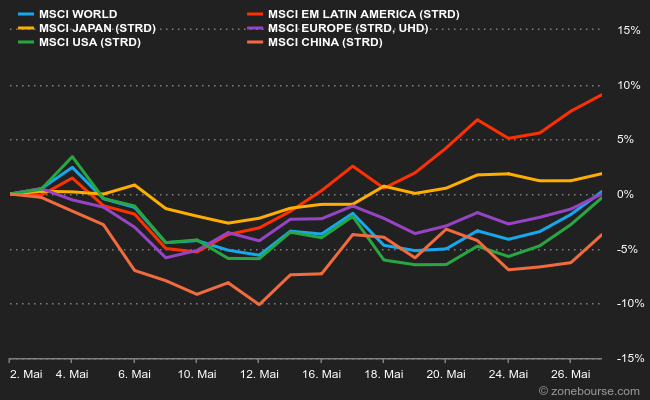

Regional trends: Latin America in the lead, China at the bottom

May started badly for indexes, but it looks like it will end well. Regional performances are close to balance for Europe and the US, while Latin America is clearly back on track. China is still hampered by Covid restrictions.

.

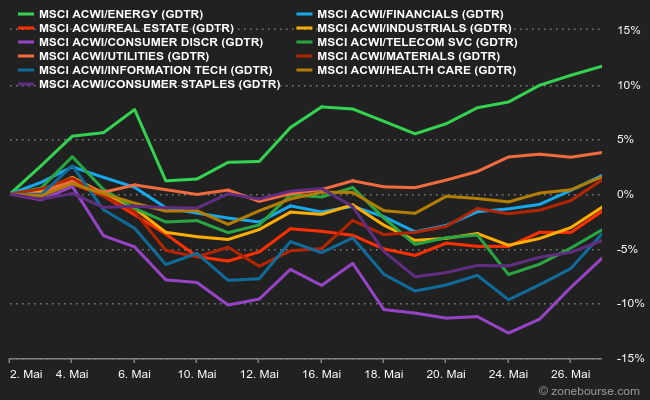

Sectoral Top / Bottom: tech and consumer cyclicals rebound

At the sector level, there is no stopping oil stocks. The MSCI Energy Index has gained more than 10% since the beginning of May. In recent sessions, however, there has been a marked return of the two unloved commodities of 2022: consumer discretionary and technology

.

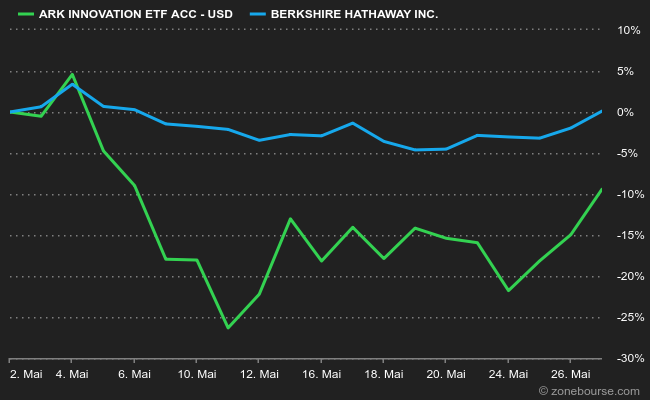

Illustration with our favorite indicator of risk appetite, the track record of Cathie Wood's ultra-risky ARK Innovation fund (green) versus the track record of Warren Buffett's Berkshire Hathaway (blue). The hare rallies at the end of the month, while the tortoise stays ahead.

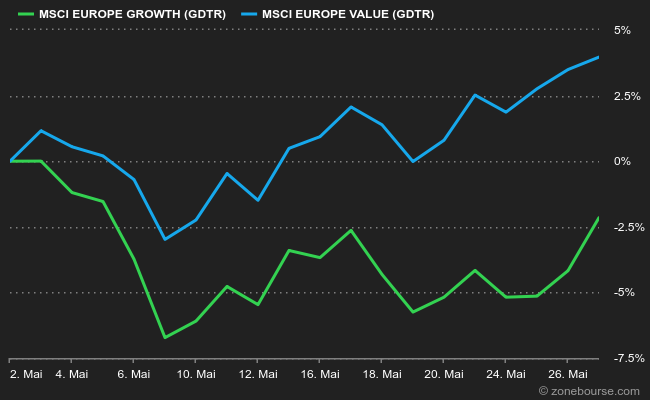

Another version of investor habits with the Value (low P/E stocks, in blue) vs Growth (growth stocks, in green) match in May. If growth rebounds at the end of the month, financiers do not seem to have abandoned their value bets

.

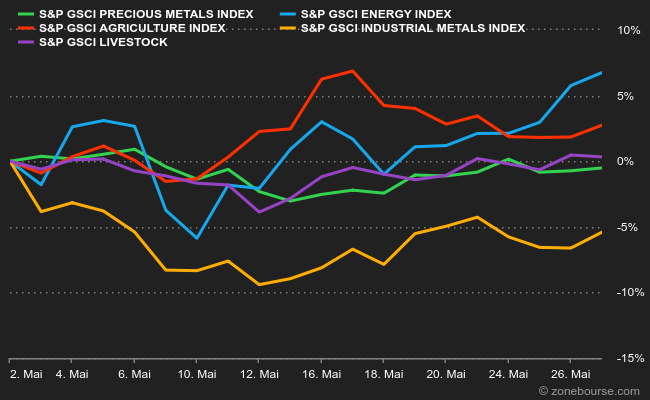

Commodities: energy still shines

Let's go to the commodities market. Industrial metals are still down for the month of May, due to fears about the strength of growth. Energy is still in the spotlight, while agricultural prices keep rising, even if the increase has moderated since mid-May. Precious metals are not exciting the crowds.

.

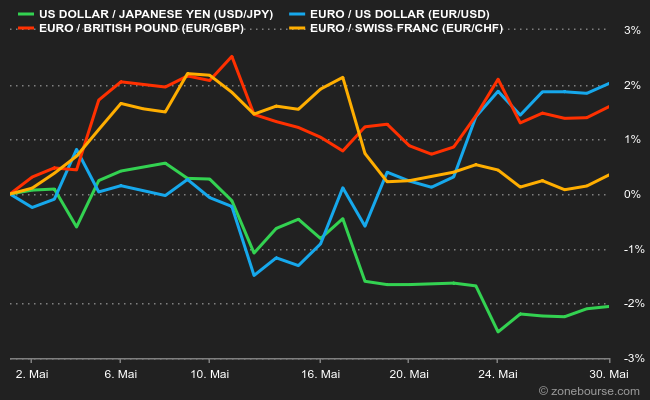

Currencies: the euro emerges from its torpor

We end this panorama with the foreign exchange market, where the euro is a little more active than in recent weeks, following the ECB's hawkish comments.

.