|

Monday June 22 | Weekly market update |

| Despite a spike in Covid-19 cases in the United States and China, last week was rather good for financial markets, which took advantage of new support measures announced by the Fed to regain some ground. The further acceleration in oil prices is another supporting factor. |

| Indexes All indices have recovered some losses last week. In Asia, the Shanghai Composite regained 1.6%, the Hang Seng 1.3% and the Nikkei 0.8%. In Europe, the gains are more significant after the four witches. The CAC40 and Dax gained 3.2% and the Footsie with 2.8%. For the peripheral countries of the euro zone, Portugal gained 2%, as did Spain and Italy, which gained 1.8% and 3.3% respectively. In the United States, the Dow Jones recorded a weekly performance of 2.5%, the S&P500 climbed 3.1% and the Nasdaq100 outperformed by 4.5%, following its historical highs. |

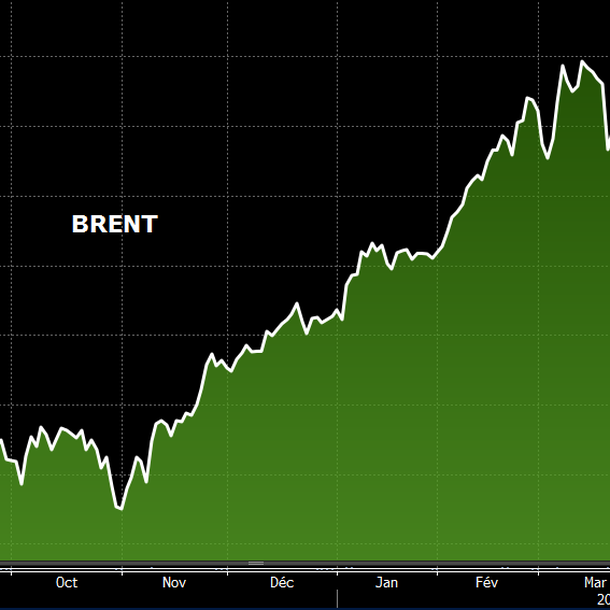

| Commodities Oil prices remained on an upward trend last week, supported by improved demand conditions while OPEC+ members reaffirmed the paramount importance of respecting production agreements. Meeting within the framework of the OPEC Agreement Monitoring Committee, countries that have not respected their quotas are being asked to make up their shortfall over the coming months. It should be noted that Moscow does not consider it necessary to further limit production after July. Brent is up 8.5% to USD 42.5, as is WTI at USD 40. The price of gold is stabilizing close to its peaks at USD 1735, still sought after by investors. Silver borrows the same momentum and lags at USD 17.7. Industrial metals recorded a positive weekly sequence, like lead and aluminum, which rose by 3.5% and 1.9% respectively to USD 1796 and USD 1586 per metric ton. Brent continues its rebound  |

| Equities markets Shimano Founded in 1921, Shimano is a Japanese family business dedicated to the manufacture and sale of bicycle components and fishing equipment. With the Covid-19 crisis, people around the world are increasingly adopting bicycles as a means of transportation. In fact, bicycle sales have exploded in Europe after lockdown restrictions ended. The European market represents 40% of its sales. Shimano is therefore on the right track and intends to take advantage of the growth prospects offered by the cycle market. Since its low in March, the Japanese manufacturer's share price has exploded by 66%, giving rise to a positive configuration, allowing it to gain 19% over 2020. Shimano's share price had fallen by 28% at the beginning of the year, after the company reported a 3.9% decline in net income for 2019. Shimano (capitalization of 18 billion dollars) will celebrate its centenary next year. In addition, there is still great potential for innovation, with bicycle components linked to the heart rate of cyclists. Shimano also has a very healthy financial situation with a net cash position equivalent to 2.2 billion euros in 2019 and will therefore have no difficulty in financing R&D. After 5 years in the same zone, Shimano's stock soars  |

| Bond market Faced with a new set of weak U.S. labor market numbers, many investors headed to the safe haven of government securities on Thursday. The bond market barometer saw the Bund's yield fall back to -0.41%, just behind the Swiss benchmark, which retains its earnings base at -0.47%. For its part, the same path is taking shape for the French OAT, symbolically leaving positive territory at -0.07%. The fall in yields is being seen in all countries. The surprise comes once again from Greece, which sees its 10-year rate fall to 1.26%, below the Italian rate at 1.37%. Yield spreads are traditionally highly correlated with country ratings, except in the case of Italy, which seems to be at levels corresponding to a rating of BB-, whereas its official rating is BBB. In the U.S., the Tbond is trading at 0.71%. If the U.S. economy were to recover further between now and the fourth quarter, the presidential election campaign could cause uncertainty in the bond market with a risk of approaching 1%. |

| Forex market Sterling's weakness is well known against all its counterparts. This deterioration follows the Bank of England's new intervention (liquidity injections). The USD/GBP is trading on a basis of USD 1.24(-300 basis points for the past two weeks). The EUR/GBP is also positioning itself in a bullish pattern and triggers a new chart acceleration beyond GBP 0.90. The safe havens that have been left behind since the V-shaped recovery hopes with the reopening of economies are once again dominating long positions for Forex traders, with the potential for a second wave of health care in China. The yen maintains its hegemony against the greenback at JPY 107 and the Swiss franc is trading in a more revised price zone since the bottom of the crisis at CHF 0.945 (-150 bps). The SNB renewed its commitment to an ultra-expansive monetary policy, saying its unconventional measures will help Switzerland cope with its worst recession in decades. The euro is struggling to confirm its bullish start against the dollar and is returning to the USD 1.1210 zone on contact with its 20-day bullish average. The release of good U.S. statistics has eroded the single currency. As for emerging currencies, the Argentine peso is going through difficult times, with the Buenos Aires currency gradually weakening against the dollar. The government defaulted last month on the country's foreign debt. Some of Argentina's largest creditors presented a new debt proposal to the government this weekend as the two sides move closer to a $65 billion restructuring deal. Argentinian peso falls against the dollar  |

| Economic data Few statistics were on the agenda in Europe, but overall they exceeded expectations, as the German Zew index came out at 63.4 compared to 51 last month. In the Euro-Zone, the CPI index came out as expected at +0.1% and the current account balance at 14.4B. In the United States, retail sales jumped by 17.7%, industrial production rose by only 1.4% (consensus 3%) but was down 12.5% in May. The other positive surprises were the leading indicators, which returned to green for the first time in 3 months (+2.8%) and the Phillyfed index, which rose to 27.5 (consensus -23). This week, traders will take note of the Flash PMI manufacturing and services indexes, durable goods orders, and the latest estimate of U.S. GDP for the second quarter, before household spending and income and the Michigan confidence index. In the euro zone, the Flash PMI manufacturing and services indexes will be unveiled on Wednesday, along with the German IFO. |

| The truth usually lies somewhere in the middle If markets had overreacted in the downturn, they probably experienced an exaggerated surge of euphoria in the recovery movement, going so far as to break new records for the Nasdaq100. The pendulum is swinging in the right direction. These excesses of judgment create volatile and very abrupt trajectories, and the truth is certainly in the middle. Indices try to find a balance between the hopes of a V-shaped or less assertive, square-rooted recovery and persistent health fears. In this complex environment, investors must therefore be highly selective in order to position themselves on the winning stocks, whatever the scenario. |