|

Monday October 19 | Weekly market update |

|

European markets have experienced another turbulent week, caught up by the expansion of Covid-19, prompting further partial lockdowns in several countries. Risk appetite has dissipated, with renewed caution on the part of investors, all the more so with the stalled negotiations on the American recovery plan and the first quarterly publications greeted with little enthusiasm in the United States. Prudence should continue to be the order of the day as we await the next corporate results and the US presidential election. |

| Indexes Over the past week, major indices have evolved in scattered order. Asia fared well, with a contained decline of 0.9% for the Nikkei. The Hang Seng, for its part, gained 1.2% and the Shanghai Composite 1.9%. In Europe, thanks to Friday's rebound for the three witches, the CAC40 remained stable, the Dax was down by 0.9% and the Footsie by 1.6% in the face of uncertainty surrounding the Brexit. For the peripheral countries of the euro zone, Spain lost 1.7%, Italy 0.9% and Portugal rose 0.6%. On the other side of the Atlantic, quarterly results, which were generally higher than expected, were for the most part sanctioned, particularly in the banking sector. The Dow Jones was up 0.6%, the S&P500 up 0.8% and the Nasdaq100 up 2.1%. Nasdaq100 maintains momentum  |

| Commodities Crude oil prices ended the week in balance. The rebound in early October is struggling to be sustained, due to persistent threats to oil demand. The intensification of the second wave of Covid-19 around the world is rightly worrying traders as new restrictive measures are multiplying. Brent is trading at USD 42.5 while WTI is trading at just over USD 40 a barrel. The week got off to a bad start for gold, the price of which fell following US inflation figures, which are not accelerating despite all the ultra-accommodating measures taken by the Federal Reserve. Nevertheless, the increased volatility of equity markets, penalized by the pandemic, allowed the gold metal to regain a little more height at the end of the week. As a result, gold is still trading above USD 1,900. Silver also lost some ground at USD 24.2. As for base metals, they ended up in scattered order. Copper and lead declined to USD 6680 and $1754, while aluminum and nickel posted a positive weekly performance at $1824 and $15350 per ton. |

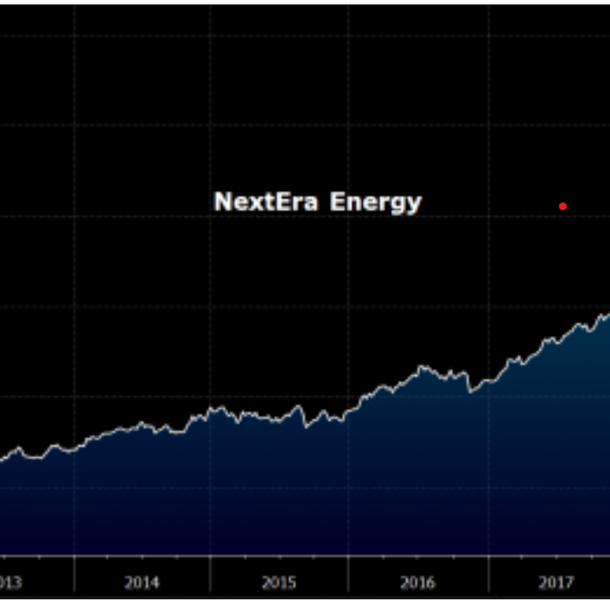

| Equities markets NextEra Energy is specialized in the production and distribution of electricity. The company is divided into three main segments: - Florida Power & Light Company which serves more than 5 million customers in Florida. - Gulf Power Company, which serves approximately 470,000 customers in eight Florida counties. - NextEra Energy Resources which is a renewable energy producer (wind and solar) with a total capacity of 14,400 MW (30% of revenues). Despite the health crisis, NextEra Energy reported an 11% increase in profits for all its activities in the second quarter of 2020. Moreover, with a net debt to EBITDA ratio of 4.39x in 2019, NextEra is relatively indebted. Nevertheless, if we make a comparison with its main competitors (Duke Energy, Dominion Energy, Southern Company, American Electric Power), we notice that the sector average is 5.13x in the same year. On the other hand, if we take a look at NextEra's CAPEX/CA ratio, with 55.8% in 2019, it is among the highest in the sector (average at 40.9%), which may affect its financial situation. The industry is therefore highly capital intensive. Nevertheless, NextEra stands out widely on the stock market. While the Florida-based company recorded a latent performance of 23% over the year, its competitors, mentioned above, are mostly progressing backwards. This progress has enabled NextEra to reach a market capitalization of $147 billion, exceeding the value of traditional supermajors such as Chevron or Exxon Mobil. At the same time, this phenomenon underscores the paradigm shift we are witnessing today, namely a structural shift in energy values towards more renewable energy. Momentum bullish on NextEra Energy which realizes +440% over 10 years  |

| Bond market Euro zone bond markets have shown a classic pattern of risk aversion. The yield of the bund returned to a historic low of -0.61% and that of the French OAT to -0.34%. It is a first in a long time to see the German yield below that of the major Swiss bond at -0.59%. In the Mediterranean region, countries are also benefiting from this additional easing movement. Italy borrows at 0.67% while Spain and Portugal benefit from unprecedented conditions, financing their public spending with a rate of 0.13% over 10 years. Even if data from the euro zone is very scarce, attention is focused on the Brexit negotiations, the outcome of which remains more than uncertain. Although both parties seem to be stubborn, communication is still open. The continued strength of the bond market barometer will probably depend for the time being on the outcome of the negotiations in Brussels in particular. In the United States, the Tbond is trading on a yield basis at 0.72% pending the US elections and a forthcoming stimulus plan. |

| Forex market The dollar rose against all the pairs in the Group of 10, in an anxiety-inducing health environment. The single currency was weakened by the outflows of foreign exchange traders. The major EUR/USD parity is trading close to USD 1.173, a two-month low. The euro also declined against the yen to JPY 123.5 (-150 basis points). In a context of risk aversion, safe-haven currencies are gaining ground. The Japanese currency and the Swiss franc are accumulating weekly gains against a majority of currencies. The flows are essentially one-way as short-term bettors are not looking to smooth the moves for the time being. In the United Kingdom, the pound sterling is experiencing erratic movements. The British currency is trading at USD 1.30 against the bill and GBP 0.90 against the euro as London moves to a higher level of restrictions on socialization. In addition, during the European summit negotiations, the EU and the UK failed to make a clear breakthrough in discussions on a future trade agreement. In Asia, the yuan continues its forward march to trade at CNY 7.90 against the single currency and CNY 6.72 against the greenback (see chart). In the southern hemisphere, the Australian dollar declined after RBA Governor Lowe said the central bank was questioning whether buying longer-term bonds would help boost jobs. Yuan rebounds against the dollar  |

| Economic data In China, statistics missed the consensus last week. The trade balance stands at 258B (consensus 420B) and the PPI and CPI indices are below expectations at -2.1% and 1.7% respectively, while the market was expecting -1.9% and 1.9%. The same observation was made in Europe, despite the lack of news. Industrial production rose by 0.7% in the euro zone (0.8% expected compared with 5% last month). The CPI index (consensus -0.3%) and the trade balance (18.1B expected). In the United States, the figures were more mixed. Disappointments came from weekly unemployment registrations at 898K or manufacturing activity in the New York area (10.5 against 17 previously), while the CPI index and import prices were in line with expectations (at +0.2% and +0.3%) while the PPI index recovered to 0.4% (consensus 0.2%). On Friday, retail sales rebounded by 1.9% (0.7% expected), industrial production fell by 0.6% (+0.6% expected) and Michigan's confidence index came out at 81.2 (consensus 80.2). This week, data will focus on data from China (GDP, industrial production, retail sales, unemployment rate) and then on the Fed's Beige Book, before the Flash PMI manufacturing and services indexes in the euro zone and across the Atlantic. Today, data showed that after 3.2% growth in the second quarter, Chinese GDP accelerated to 4.9% in the third. This is a little less vigorous than expected, but the slope is clearly reversed. |

| ECB's strong support In Europe, the economy will once again be held back by political decisions aimed at protecting the health of the population. In the US, restrictions cause the country to spend without measure, creating a historical debt. These exceptional conditions remain possible thanks to the very lax monetary policy of central banks. The ECB's absorption of net public debt issues amounts to 50%, the limits being pushed back for the umpteenth time. |