Ambiance: Finally some good news! For the first time in months, US inflation is cooling. Investors roared with pleasure at this announcement, especially for the benefit of highly leveraged stocks. But they did not roar for long, as if they needed confirmation to continue the rebound that began in July. Thursday's announcement of lower producer prices could have been that confirmation, but it wasn't really the case. Still, price normalization is an important step to improve macroeconomic visibility.

Rates: The yield curve is still inverted in the United States, where the yield on the 10-year maturity is 2.85%, compared with 3.19% for the 2-year. The market is sticking to its guns, believing that short-term economic conditions are deteriorating. It's hard to argue with that. But the publication of less vigorous inflation than expected in July has caused a downward revision of projections for a rate hike: the majority of the market is counting on a 50-point rate increase by the Fed in September, instead of a 75 basis point one. In Europe, the ECB is working to avoid an increase in the spread between German (0.95%) and Italian (3.03%) debt. The French OAT is at 1.52% over 10 years.

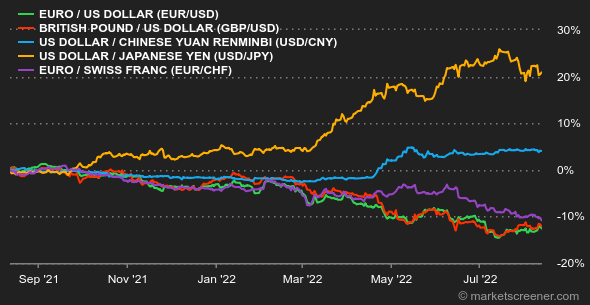

Currencies: The euro has regained some color against the dollar. It is back at USD 1.03, a level it had sunk to in early July. However, the single currency remains down 9.5% since the beginning of the year and is also suffering against the franc, at CHF 0.9705. The greenback lost ground against the major currencies after the release of inflation figures on Wednesday, which suggest a potentially shorter-than-expected monetary tightening cycle. The Dollar Index fell back to around 105 points.

Cryptocurrencies: In the wake of U.S. stock indexes, bitcoin continued its ascent this week and is now hovering around $24,000 as of this writing. For its part, ether is clearly outperforming the market leader, rising 6 times since the beginning of August. ETH is thus back to sailing around the $1,900 mark after having passed under the psychological threshold of $1,000 in June. A crazy progression that can be explained above all by a renewed appetite of investors for risky assets in recent weeks.

Calendar: The main statistic of the next week is expected on Wednesday with the July retail sales in the United States. On the same day, the U.S. central bank will release the detailed minutes of its latest meeting. Other highlights include Chinese retail sales (Sunday night) and UK inflation for July (Wednesday).

|